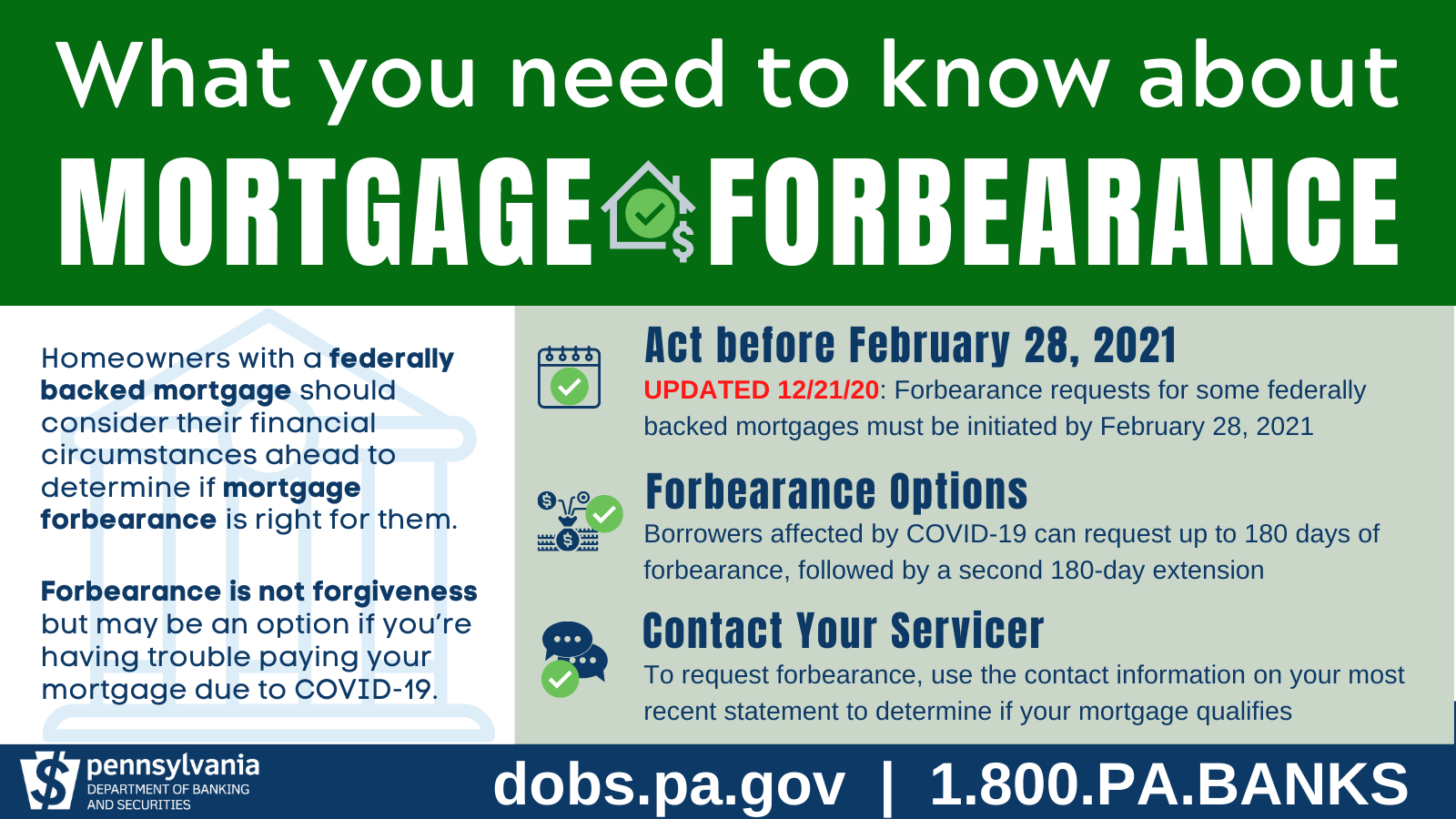

UPDATE 12/21/2020: USDA and FHA extend the deadline for initiating CARES Act forbearance claim to February 28, 2021.

The end of each year tends to bring about a sense of completing various tasks before the New Year rings in, and this year is certainly no different.

For homeowners, it's important to know that February 28, 2021 is the deadline to take advantage of forbearance options for some qualifying mortgages under the CARES Act. The CARES Act also prohibits negative credit score reporting for homeowners utilizing this pandemic forbearance option.

If you are a borrower with a federally backed mortgage, meaning your mortgage is guaranteed by a federal government agency like Fannie Mae, Freddie Mac, USDA, FHA/HUD, VA, or Ginnie Mae, you have a right to request and obtain a forbearance for up to 180 days if you are directly or indirectly affected by Covid-19. You also have the right to request and obtain an extension for up to another 180 days (for a total of up to 360 days).

Forbearance is not forgiveness and any missed payments will need to be paid back, but it could be a suitable option for those experiencing difficulty making their full monthly mortgage payment.

You must contact your loan servicer to request this forbearance. There will be no additional fees, penalties or additional interest (beyond scheduled amounts) added to your account. You do not need to submit additional documentation to qualify other than your claim to have a pandemic-related financial hardship. It's important to note that this is intended as a broad definition to be as accessible as possible

Additionally, financial regulators have clearly communicated to mortgage loan servicers that balloon payments, as in all past due amounts, are not required at the conclusion of the forbearance period. Regulators have given servicers broad leeway to be able to pursue more flexible repayment options, such as reduced payments or adding missed payments to the end of the loan.

Homeowners that are uncertain about their financial condition in 2021 should consider forbearance options, should their situation change after the deadline.

For example, if you have experienced an indirect financial hardship in the past nine months from higher grocery bills, or unanticipated purchases of equipment for remote work or your children's education, you may be able to make your full mortgage payment currently. By communicating to your servicer that you'd like to receive a forbearance, you can protect against any change in your situation in the New Year.

Homeowners that can continue to make a full mortgage payment should continue to do so. For those uncertain about their economic future, they may choose to put their monthly payment into a savings account. When the period of forbearance ends, they'll be able to pay the full amount in forbearance and resume regularly scheduled payments.

Here's what homeowners uncertain about their ability to make their mortgage payment should do today:

- Determine if your mortgage loan is federally backed. The easiest way is to contact your loan servicer through contact information provided on your most recent monthly statement.

- If your mortgage qualifies, and you've been directly or indirectly affected, communicate to your servicer that you are requesting a Covid-19 forbearance. Some servicers may provide an initial three-month forbearance, or month-to-month, but you have the right to request up to 180 days.

February 28, 2021 (Updated 12/21/2020)

- For homeowners already enrolled in a forbearance agreement, continue to communicate with your servicer. Understand your rights under the CARES Act and exercise them, but also remember that communication is key to staying in your home.

- Contact the Department of Banking and Securities at 1-800 PA Banks if you have any questions, concerns or complaints about your mortgage or any other financial matter.

Remember:

- Forbearance is not forgiveness; you will still owe any missed payments but there are numerous repayment options available.

- This forbearance is for federally backed mortgages, but other options may be available for non-federally backed mortgages.

- Communication with your servicer is key.

Additional Resources:

CFPB – What is a forbearance?

https://www.consumerfinance.gov/ask-cfpb/what-is-forbearance-en-289/

Guidance to Servicers

https://files.consumerfinance.gov/f/documents/cfpb_csbs_industry-forbearance-guide_2020-06.pdf

Sample Forbearance Script (What to Expect When You Call)

https://singlefamily.fanniemae.com/servicing/covid-19-forbearance-script-servicer-use-homeowners